For today’s merchants, fast, secure, and reliable payments are no longer a differentiator; they are the minimum expectation. As card-not-present fraud continues to rise and issuers apply more sophisticated risk models, the way payment credentials are stored and transmitted has become critical to performance.

Network tokens have quietly moved from an optional enhancement to a foundational requirement of modern payment systems. Merchants that still rely on raw card numbers or legacy tokenization models are seeing lower approval rates, higher fraud exposure, and increasing compliance complexity. In today’s payment landscape, modern payments simply do not work without network tokens

What are Payment Tokens?

Before understanding network tokens, it’s important to understand payment tokens first.

Payment tokens are a security technique that replaces sensitive card data such as a credit card number (PAN) with a non-sensitive placeholder called a token. This token has no exploitable value on its own and cannot be reverse-engineered to reveal the original card number.

Instead of storing or transmitting real card numbers, businesses store and process tokens. This dramatically reduces the risk of data breaches and helps limit PCI compliance scope, since sensitive card data is no longer sitting inside merchant systems.

In practice, tokenization ensures that real card details are never exposed during normal business operations, making it a foundational security layer for modern payments.

What are Network Tokens?

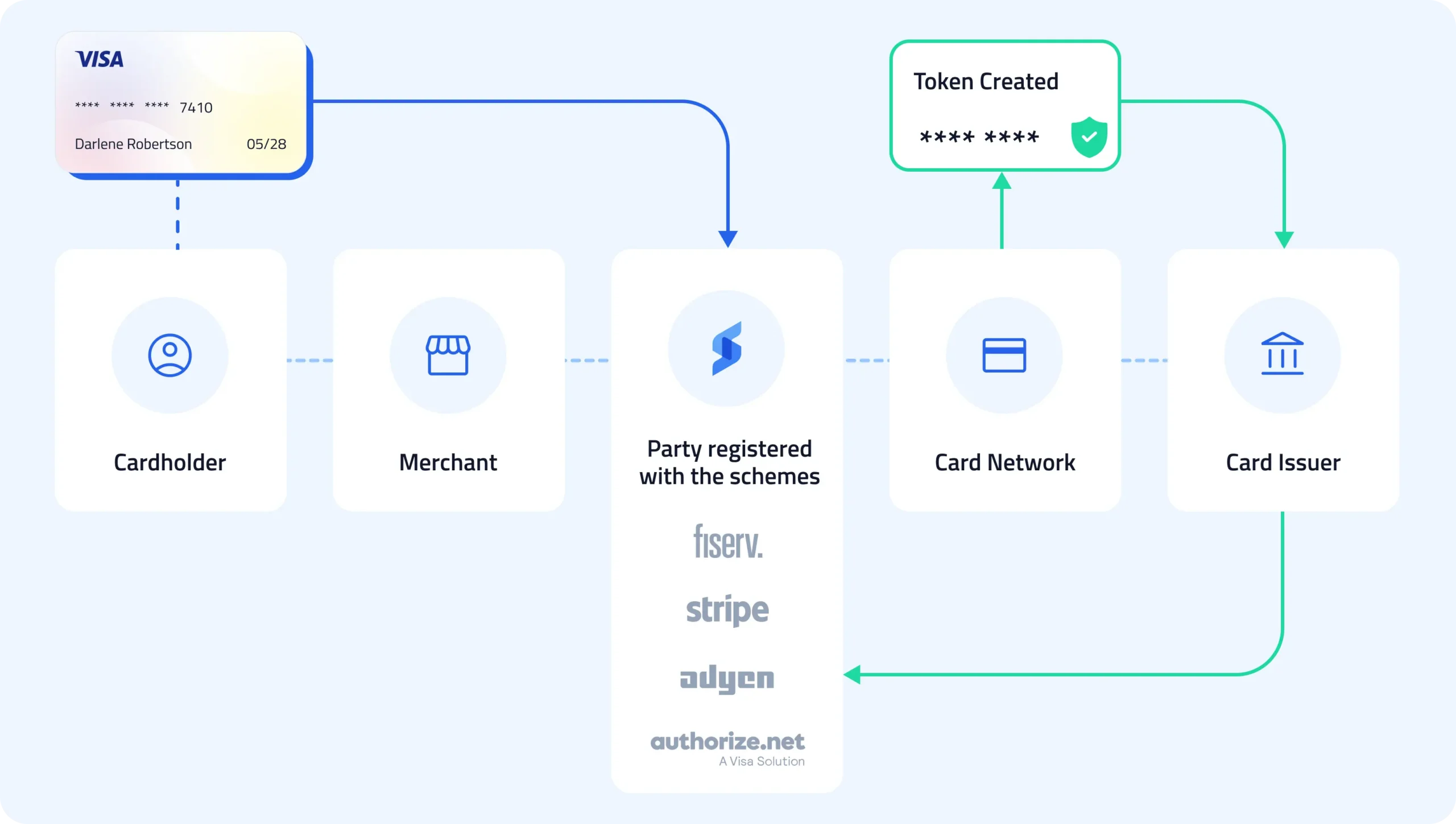

Network tokens is the process of replacing a customer’s primary account number (PAN) with a secure, card-network-issued token. This token is unique to the merchant and transaction context and is recognized across the entire payment ecosystem.

For the consumer, it feels seamless. For the merchant, it means higher approval rates, fewer failed payments, lower churn, and stronger issuer trust. This is exactly why network tokens have become the standard for modern, high-volume digital payments and why merchants that don’t use them feel outdated by comparison.

Unlike gateway or processor tokens, network tokens are issued and managed by the card networks themselves including Visa, Mastercard, American Express, and Discover. Because they travel through the networks, they enable richer data sharing with issuers and stronger transaction trust.

Network tokens also support automatic credential updates when cards expire, are reissued, or change eliminating a common cause of failed payments.

You’ve Likely Already Used Network Tokens

If you’ve ever watched Netflix uninterrupted after getting a new credit card, or upgraded your iPhone using Apple Pay without re-entering your payment details, you’ve already experienced the power of network tokens.

Behind the scenes, these companies rely on network tokenization to ensure stored payment credentials automatically update when cards expire, are reissued, or change. Instead of prompting you to update your card or risking a declined payment, the token refreshes securely through the card networks, keeping the transaction flowing without friction.

Why Network Tokens Are Now a Requirement for Modern Payments

Issuers increasingly expect ecommerce, subscription, and stored-credential transactions to be tokenized. Network tokens signal lower fraud risk and higher transaction integrity, which directly influences authorization decisions.

As issuer models evolve, non-tokenized card-not-present transactions are more likely to be declined even when customers are legitimate. This shift has made network tokenization a baseline requirement rather than an optimization.

Merchants that have not adopted network tokens are already operating at a structural disadvantage in today’s payments ecosystem.

How Network Tokens Improve Authorization Rates

Network tokens improve authorization performance by increasing issuer confidence. Tokenized transactions benefit from:

- Higher issuer trust

- Enriched transaction metadata

- Automatic card lifecycle updates

This is especially important for subscriptions, marketplaces, and repeat purchases, where outdated card credentials often lead to unnecessary declines. Network tokens create a self-healing payment lifecycle, reducing failed transactions without requiring customer intervention.

Without network tokens, merchants rely on static PAN data that degrades over time directly impacting revenue.

Built-In Fraud Reduction Without Checkout Friction

Network tokens are inherently more secure than raw card numbers. They are merchant-specific, domain-restricted, and unusable outside their intended context. Even if intercepted, a network token cannot be reused elsewhere.

When combined with authentication solutions like 3D Secure, network tokens allow merchants to reduce fraud while preserving a seamless checkout experience. This layered approach protects transactions without introducing unnecessary friction for trusted customers.

Simplifying Compliance and Reducing PCI Scope

Storing and transmitting raw PANs increases PCI scope, audit complexity, and breach risk. Network tokenization removes sensitive card data from merchant environments, significantly reducing compliance exposure.

For growing businesses, this means:

- Lower compliance costs

- Reduced operational risk

- Faster scalability across channels

Network tokens make strong security and compliance practices achievable without slowing growth.

Network Tokens Enable the Future of Payments

Modern payment strategies such as payment orchestration, multi-processor routing, digital wallets, and AI-driven authorization optimization depend on network tokenization.

Because network tokens are processor-agnostic, they allow merchants to:

- Route transactions dynamically

- Avoid vendor lock-in

- Expand into new channels faster

Without network tokens, payment stacks become rigid and increasingly difficult to evolve.

The Cost of Not Using Network Tokens

Merchants that delay network token adoption often experience:

- Lower approval rates

- Higher fraud exposure

- Increased subscription churn

- Greater compliance overhead

- Limited payment flexibility

In today’s environment, not using network tokens is not a neutral choice, it is a competitive liability.

Final Thoughts: Modern Payments Require Network Tokens

Network tokens are no longer a premium feature or future innovation, they are core payment infrastructure. As networks and issuers continue to raise expectations, tokenization has become the standard for secure, high-performing payments.

Merchants that adopt network tokens gain higher approvals, lower fraud, simplified compliance, and long-term flexibility. Those that do not will increasingly struggle to compete in a modern payments ecosystem.

Build Modern Payments on Network Tokens

SeamlessPay delivers processor-agnostic network tokenization designed to increase approval rates, reduce fraud, and support scalable payment orchestration without locking you into a single provider.

Modern payments don’t work without network tokens. SeamlessPay ensures you’re built for what’s next.