Tokenization has become one of the most important security and infrastructure layers in modern payment systems. Instead of transmitting or storing a card’s Primary Account Number (PAN), payment platforms replace sensitive card data with tokens that act as secure substitutes. This approach significantly reduces fraud risk, improves compliance with PCI DSS requirements, and protects merchants from storing highly sensitive cardholder data.

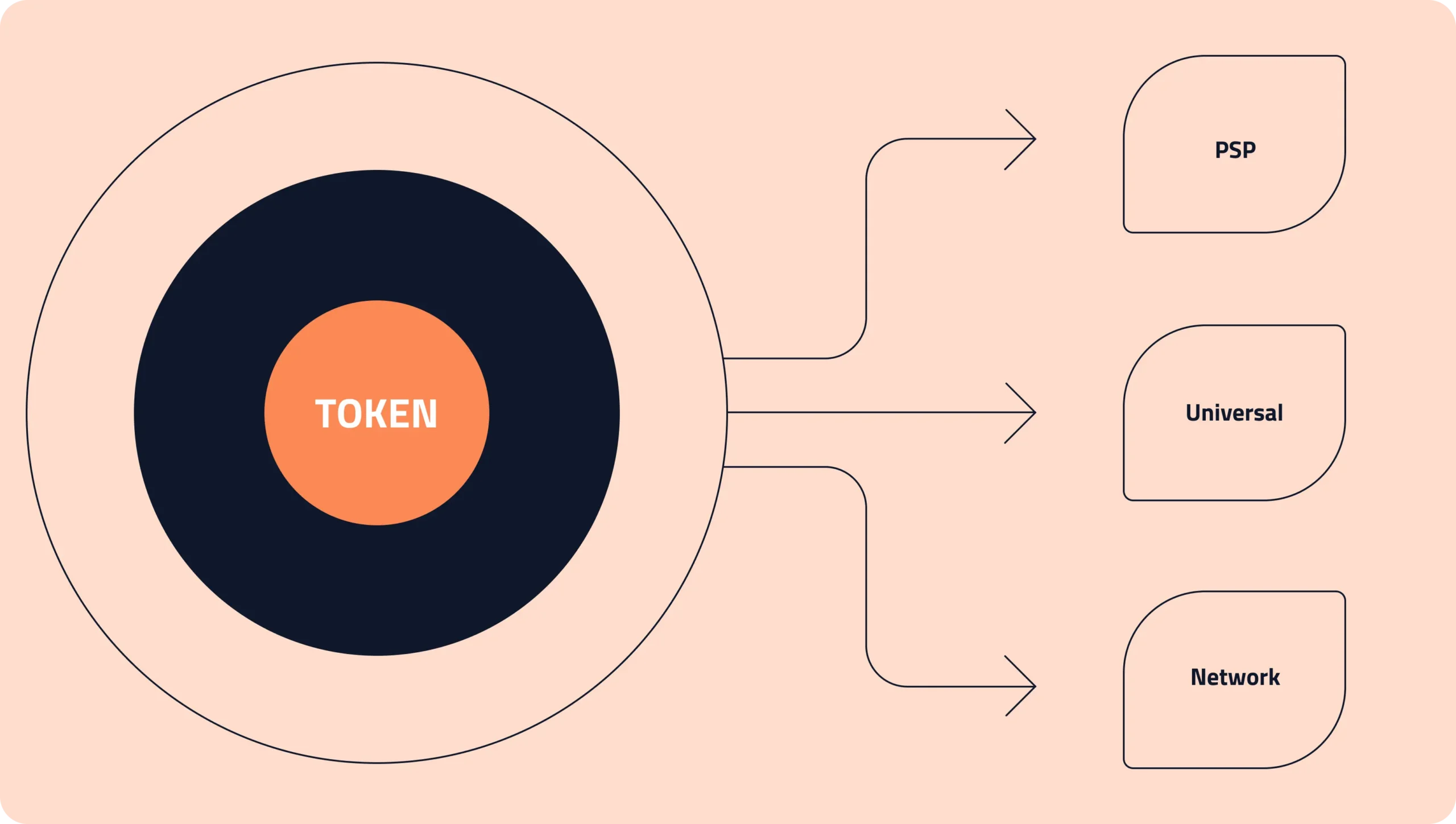

However, not all tokens function the same way. Different tokenization models determine who controls the token, where it can be used, and how portable it is across payment systems. The three most common types used in modern payments are PSP tokens, universal tokens, and network tokens. Understanding the differences between these token types helps businesses design more flexible payment infrastructure, improve authorization performance, and avoid vendor lock-in.

What Is Payment Tokenization?

Payment tokenization is the process of replacing sensitive payment credentials with a randomly generated identifier called a token. The token can be safely stored or transmitted without exposing the underlying card number.

When a payment needs to be processed, the token is mapped back to the original card data inside a secure token vault controlled by a payment provider, tokenization platform, or card network.

Tokenization offers several important benefits for merchants and payment platforms:

- Reduced PCI DSS compliance scope

- Lower risk of cardholder data breache

- Safer storage of customer payment methods

- Simplified recurring billing and subscription payments

- Support for omnichannel payment experiences

For example, when a customer saves their card for future purchases, the actual card number is not stored by the merchant. Instead, a token represents the payment method and is used to initiate future transactions securely.

While all tokenization methods achieve this goal, the key difference lies in who issues the token and where it can be used.

What Are PSP Tokens?

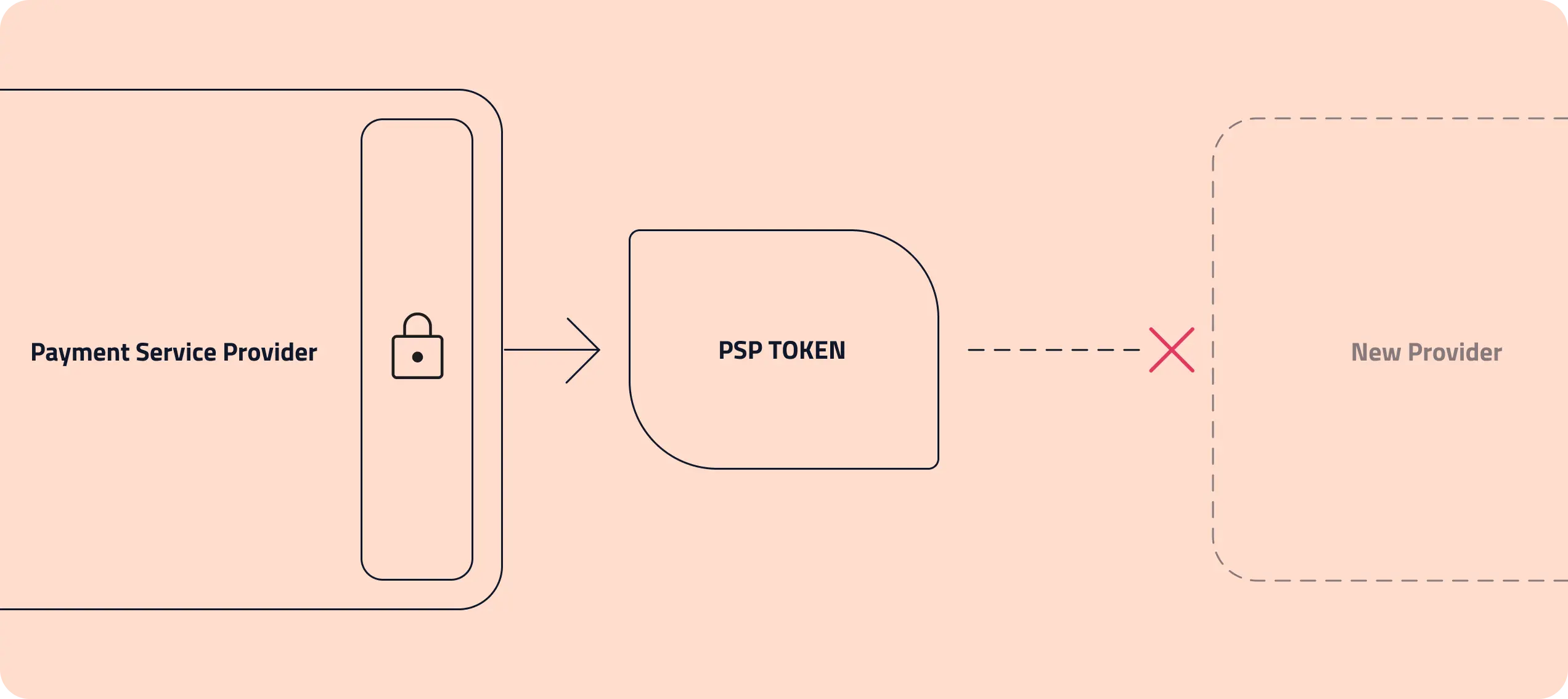

PSP tokens are tokens issued by a payment service provider or gateway. When a merchant collects card details using a PSP’s payment form, SDK, or API, the provider generates a token that represents the card within its own system.

These tokens allow merchants to store and reuse payment credentials without directly handling the raw card number. However, PSP tokens are typically tied to the infrastructure of the provider that issued them.

Key characteristics of PSP tokens include:

- Issued and controlled by a specific payment provider

- Can only be used within that provider’s platform

- Simplify PCI compliance for merchants

- Commonly used for stored payment methods and subscriptions

The biggest limitation of PSP tokens is portability. If a merchant decides to switch processors or payment gateways, those tokens generally cannot be transferred. This often forces merchants to re-collect customer payment information, which can disrupt recurring billing and cause customer friction.

PSP tokens are most common among companies that operate entirely within a single payment ecosystem and do not require complex payment routing or multi-provider setups.

What Are Universal Tokens?

Universal tokens are provider-agnostic tokens that are not tied to a single payment processor or gateway. Instead of being controlled by one PSP, universal tokens are issued by independent tokenization platforms or vault providers.

This design allows the same token to be used across multiple payment providers, gateways, or orchestration layers.

Universal tokens are commonly used in payment orchestration architectures where merchants route transactions between multiple processors for performance, cost optimization, or redundancy.

Key characteristics of universal tokens include:

- Not tied to any specific payment service provider

- Can be used across multiple processors or gateways

- Stored in independent token vaults

- Enable payment routing and orchestration strategies

Universal tokens provide much greater flexibility compared to PSP tokens. If a merchant wants to switch processors or route payments dynamically, the stored payment credentials remain usable without asking customers to re-enter their card details.

This makes universal tokenization especially valuable for large merchants, fintech companies, and payment platforms that want full control over their payment infrastructure.

What Are Network Tokens?

Network tokens are issued directly by the major card networks such as Visa, Mastercard, American Express, and Discover. These tokens replace the card number with a unique token generated by the card network itself.

Unlike PSP tokens, network tokens are not limited to a single payment provider. They are recognized across the payment ecosystem because they are managed by the card networks that process transactions.

Network tokens also introduce additional security and performance benefits.

Key characteristics of network tokens include:

- Issued by card networks rather than payment providers

- Recognized across multiple processors and gateways

- Automatically updated when cards expire or are replaced

- Frequently used in digital wallets and recurring billing

One of the most powerful advantages of network tokens is lifecycle management. If a customer receives a replacement card due to expiration, loss, or fraud, the card network can automatically update the token without requiring the customer to update their payment details.

This reduces payment failures and improves approval rates for recurring payments and subscriptions.

Network tokens are also widely used by digital wallets such as Apple Pay and Google Pay, where the card number is never directly shared with the merchant.

Comparing PSP Tokens, Universal Tokens, and Network Tokens

3DS 2.0, also known as EMV 3DS, is the modern version of the protocol, designed to improve customer experience and reduce friction seen in 3DS 1.0.

Key Upgrades Over 3DS 1.0

| Feature | PSP Tokens | Universal Tokens | Network Tokens |

| Issuer | Payment Service Provider | Independent Token Vault | Card Networks |

| Processor Portability | No | Yes | Yes |

| Vendor Lock-In Risk | High | Low | Low |

| Card Lifecycle Updates | No | Depends on implementation | Yes |

| Ideal Use Case | Single PSP integrations | Multi-processor payment orchestration | Authorization optimization and wallets |

PSP tokens are simple and convenient but create dependency on one provider. Universal tokens remove that dependency and allow merchants to control their payment routing strategy. Network tokens add another layer of security and authorization performance by leveraging infrastructure built by the card networks themselves.

Many modern payment architectures combine universal tokens with network tokens to achieve both flexibility and performance improvements.

How Tokenization Impacts Payment Performance

Tokenization is not only a security feature. It can also directly impact payment success rates and customer experience.

Network tokens in particular have been shown to improve authorization performance because they provide issuers with richer transaction data and are trusted more than manually entered card numbers.

Benefits that tokenization can provide include:

- Higher authorization approval rates

- Reduced fraud risk

- Lower PCI compliance burden

- Better performance for subscription billing

- Improved customer checkout experiences

As merchants scale and begin operating across multiple geographies, processors, and payment methods, tokenization becomes a critical infrastructure decision rather than just a security feature.

Choosing the Right Token Strategy

Selecting the right tokenization approach depends on how flexible your payment infrastructure needs to be.

Businesses operating entirely within a single payment provider may find PSP tokens sufficient for their needs. However, companies that want flexibility to switch processors or implement payment routing strategies often adopt universal tokenization.

Network tokens are increasingly becoming the industry standard for stored credentials, digital wallets, and recurring billing because of their lifecycle management and authorization advantages.

For high-growth companies, the most resilient payment architecture often combines multiple tokenization layers. Universal tokens provide portability across processors, while network tokens deliver security and performance improvements at the card network level.

Understanding how these token types interact allows businesses to design payment systems that scale with their growth, reduce operational risk, and maintain full control over their customer payment data.

Build a More Flexible Payments Infrastructure

Modern payment systems require more than just processing transactions. Businesses need infrastructure that improves authorization rates, reduces fraud risk, and allows flexibility across multiple processors and payment channels.

SeamlessPay helps businesses modernize their payment stack with tools like payment orchestration, network tokenization, intelligent routing, and fraud prevention.

If you want to improve approval rates, reduce payment failures, and future-proof your payment infrastructure, our team can help.