Online fraud is at an all-time high, and consumers expect safer, more seamless checkout experiences than ever before. To keep conversion strong—while keeping fraudsters out—merchants increasingly rely on 3D Secure (3DS), a global authentication protocol that verifies a cardholder during online and in-app payments.

3DS doesn’t just reduce fraud—it also boosts authorization rates, reduces chargebacks, and shifts liability away from merchants. In today’s digital economy, understanding how 3DS works is critical for any business processing card-not-present (CNP) transactions.

What is 3D Secure (3DS)?

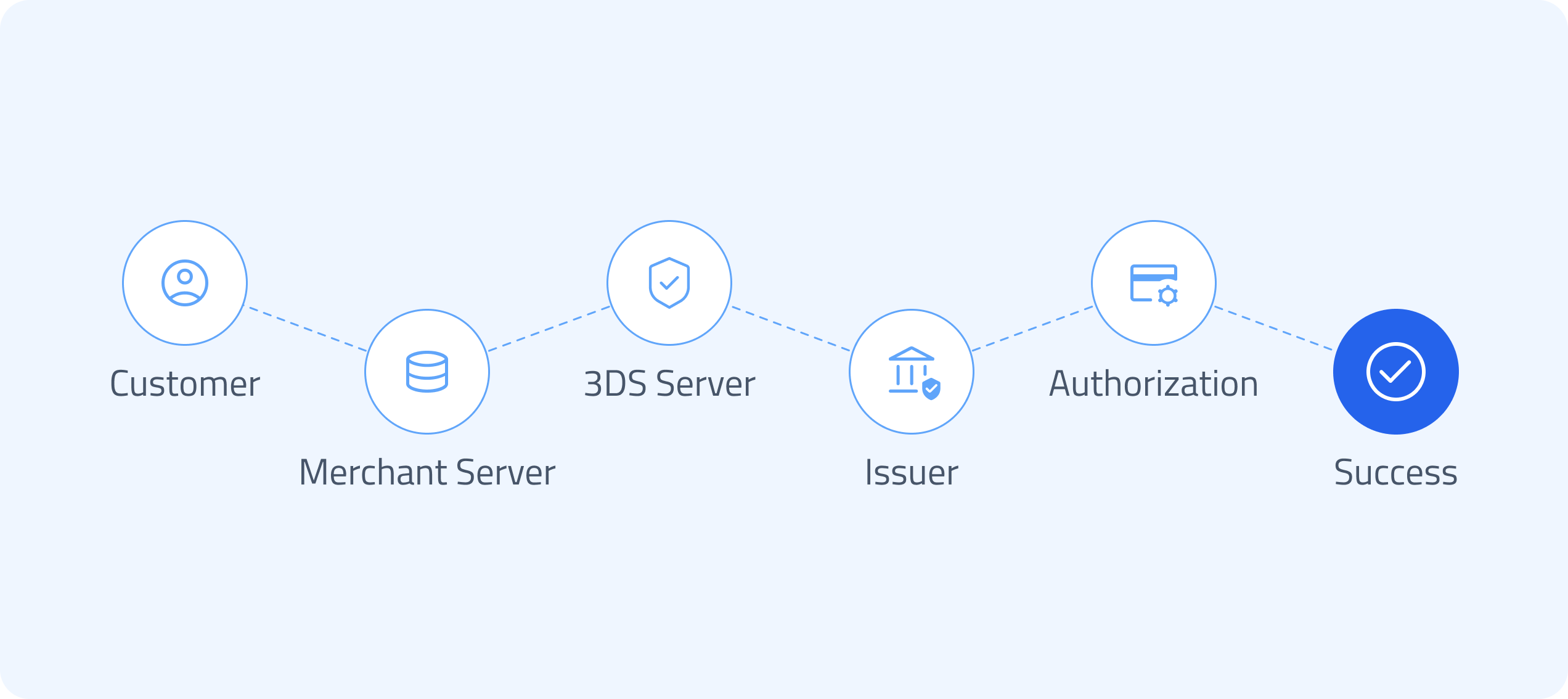

3D Secure (3DS) is an authentication protocol developed by EMVCo that confirms the identity of a shopper during online or in-app card payments. It adds a layer of security between:

- Merchant

- Issuer (cardholder’s bank)

- Card network

- Access Control Server (ACS)

When a customer checks out online, 3DS analyzes transaction data—including device fingerprints, behavioral insights, IP, shipping data, and past spending—to determine whether authentication friction is required.

3DS One-Time Password Example

If the issuer needs additional verification, the customer may be asked to confirm identity using:

- SMS one-time passcode

- Bank app push notification

- Biometrics (FaceID, TouchID)

- Banking portal login

Why It Matters

3DS helps merchants:

- Reduce fraud

- Increase authorization approvals

- Prevent friendly fraud

- Shift liability to the card issuer during disputes

For merchants using a platform like SeamlessPay, 3DS can automatically be embedded into the payment flow via e-commerce SDKs, mobile SDKs, and customizable checkout forms—ensuring smoother authentication without increased cart abandonment. SeamlessPay also offers 3DS as a standalone service that can be used with other payment processing platforms.

How Does 3D Secure 2.0 (EMV 3DS) Work?

3DS 2.0, also known as EMV 3DS, is the modern version of the protocol, designed to improve customer experience and reduce friction seen in 3DS 1.0.

Key Upgrades Over 3DS 1.0

| Feature | 3DS 1.0 | 3DS 2.0 |

| Mobile support |

Poor

Poor

|

Full native support

Full native support

|

| Authentication type |

Passwords

Passwords

|

Biometrics, push, OTP

|

| Risk-based decisioning |

Limited

|

Advanced data sharing

|

| Checkout speed |

Slower

|

Faster, frictionless

|

3DS 2.0 analyzes over 150 data points (issuing bank dependent), such as:

- Device ID

- Historical transaction behavior

- IP risk

- Transaction amount

- Shipping address consistency

- Merchant category

With these signals, most transactions are approved without requiring customer interaction, dramatically improving conversion.

Why It Matters

3DS helps merchants:

- Higher approval rates

- Fewer false declines

- Lower friction

- Better CNP fraud protection

Platforms like SeamlessPay automatically route transactions through 3DS 2.0, ensuring merchants meet card-network requirements globally.

Why Merchants Should Implement 3D Secure

1. Reduced Chargebacks

3DS shifts liability to the issuing bank, dramatically lowering risk for merchants in CNP transactions.

2. Higher Authorization Rates

Issuers approve more transactions when authentication data is included.

3. Global Compliance

Many regions—including the EU, UK, India, and parts of APAC—mandate 3DS for most online payments.

4. Lower Fraud Rates

Merchants using 3DS typically see a 30–70% reduction in fraudulent attempts (varies by vertical).

5. Better Customer Experience

3DS 2.0 creates frictionless authentication in 85–95% of transactions (network dependent).

When Is 3D Secure Required?

3DS is required or preferred in scenarios including:

- High-risk transactions (unusual device + large ticket)

- Cross-border transactions

- Repeat fraud attempts on the same merchant

- First-time shoppers

- SCA (Strong Customer Authentication) regions under PSD2

Optional exemptions include:

- Low-value transactions

- Merchant-initiated transactions (MIT)

- Trusted beneficiaries

- Corporate card rail exemptions

SeamlessPay automatically attempts exemptions to minimize friction while maintaining compliance.

How SeamlessPay Supports 3DS

SeamlessPay provides a fully integrated 3DS solution with:

- EMV 3DS authentication baked into API & SDKs

- Mobile-first flows (iOS & Android)

- Frictionless checkout via optimized issuer requests

- Risk-based authentication logic

- Reuse of tokens + 3DS data for future transactions

Merchants benefit from higher approvals, reduced fraud, and a better customer checkout experience—without lifting a finger.

Is 3D Secure Worth It?

Yes—3DS is essential for modern e-commerce. Even when not mandated, the benefits in fraud reduction and authorization performance justify implementation.

Companies processing recurring or high-value online transactions—SaaS, retail, delivery, hospitality, professional services—see outsized benefits.

Businesses leveraging SeamlessPay can deploy 3DS instantly with minimal development effort, ensuring compliance and maximizing revenue.

Conclusion

3D Secure has evolved into a powerful, customer-friendly authentication tool that protects revenue and enhances customer trust. Implementing EMV 3DS is no longer optional—it’s an essential part of a secure, modern payment stack.

With platforms like SeamlessPay, merchants can deploy 3DS effortlessly across web, mobile, and recurring billing, ensuring every transaction is secure and optimized.