What Is 3D Secure?

3D Secure is a card network authentication protocol that adds an extra verification step during checkout.

It’s branded as:

- Visa Secure

- Mastercard Identity Check

- American Express SafeKey

In addition to checking the credit card number, 3DS asks the cardholder to prove they are a legitimate user using a:

- One-time passcode

- Biometrics

- Banking app

When used correctly, 3DS:

- Reduces fraud

- Helps prevent chargebacks

- Can shift liability away from the merchant

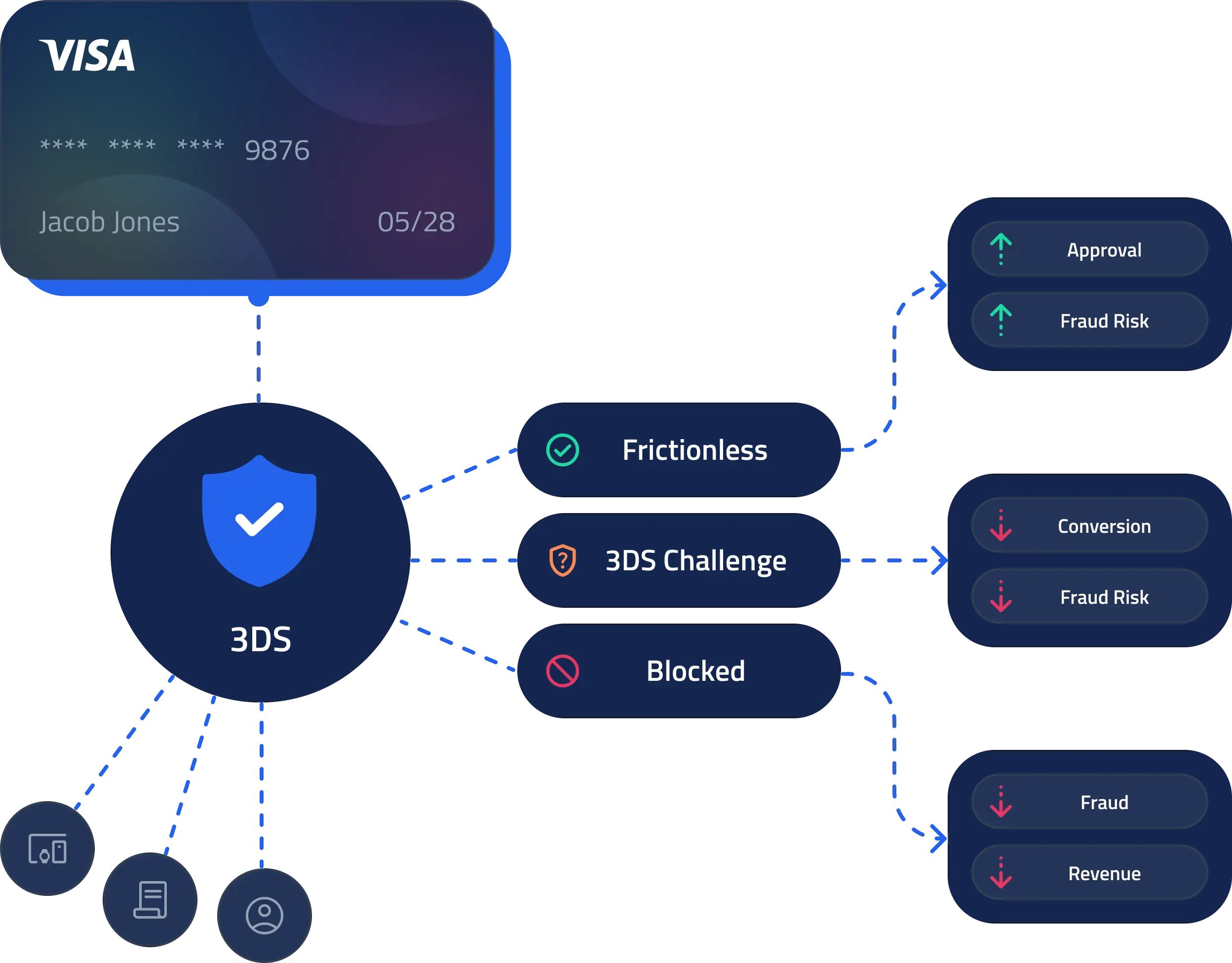

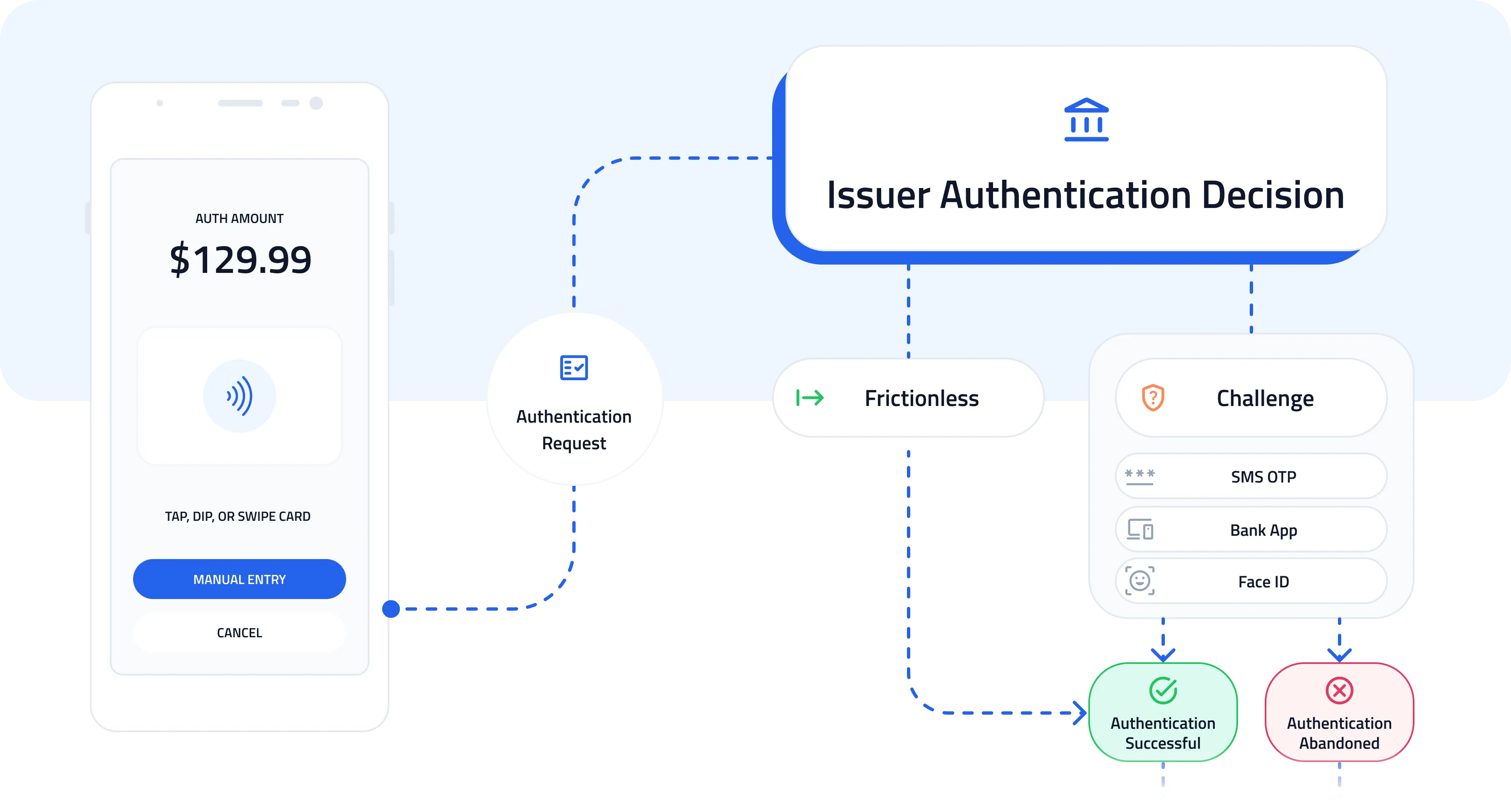

How 3D Secure Works (In Simple Terms)

- The customer enters their card

- The transaction is sent for authentication

- The issuing bank decides:

- Frictionless flow (no challenge)

- Or challenge flow (OTP / biometric)

- The transaction is approved or declined

Modern 3DS (3DS 2.0) supports:

- Frictionless flows

- Mobile-native authentication

- Risk-based decisioning

Why 3D Secure Matters More Than Ever

Card networks and banks are increasingly strict about fraud and disputes.

High fraud or dispute rates can put you into:

- VAMP

- Visa monitoring programs

- Or result in account shutdowns

This is especially dangerous for high-risk merchants.

3DS is one of the most powerful tools to:

- Reduce fraud

- Protect your ratios

- Avoid network monitoring programs

The Biggest Mistake Merchants Make With 3D Secure

Forcing 3D Secure on every transaction.

This:

- Increases friction

- Lowers conversion

- Hurts approval rates

The correct approach is adaptive 3D Secure.

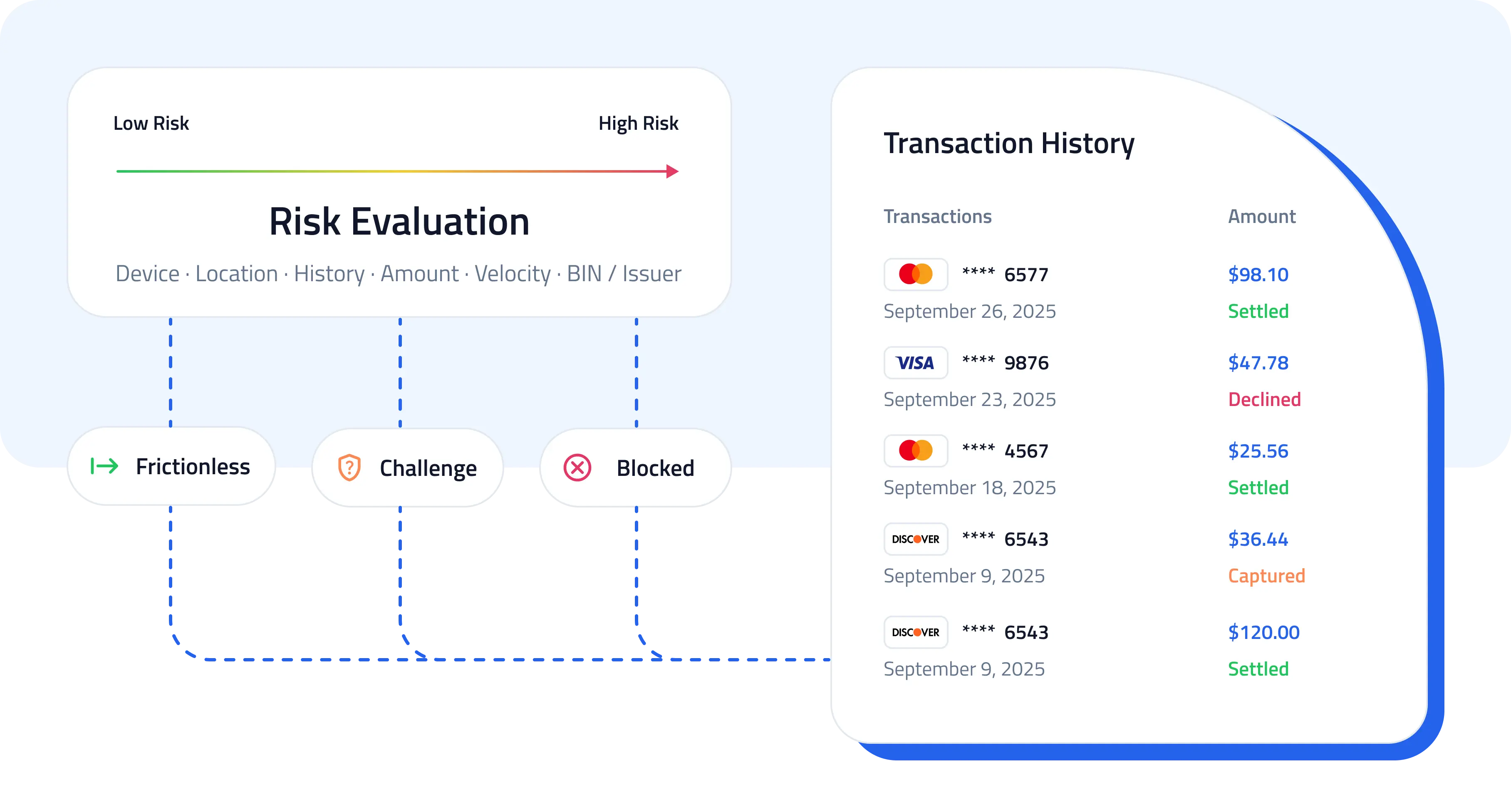

What Is Adaptive 3D Secure?

Adaptive 3DS means:

- Only challenging high-risk transactions

- Letting low-risk customers pass frictionlessly

Signals used:

- Device fingerprint

- BIN & issuer data

- Geo & velocity

- Past behavior

This approach:

- Keeps conversion high

- Reduces fraud

- Protects chargeback ratios

When Should You Use 3D Secure?

3D Secure is most valuable for:

- High-risk products

- Cross-border transactions

- New customers

- High-ticket items

- Card-not-present transactions

- Merchants close to VAMP thresholds

It is critical for:

- High-risk businesses

- Subscriptions

- Marketplaces

Does 3D Secure Reduce Chargebacks?

Yes — in three ways:

- It blocks real fraud

- It shifts liability on fraud disputes

- It discourages friendly fraud

This directly supports your chargeback prevention strategy.

3D Secure and Approval Rates

Bad implementations:

- Increase declines

- Kill conversions

- Frustrate customers

Good implementations using:

- Network data

- Smart routing

- Risk scoring

- And issuer signals

Can actually improve approval rates while reducing fraud.

How SeamlessPay Uses 3D Secure

SeamlessPay uses 3DS as part of a full payment optimization and risk engine.

You get:

- Adaptive 3DS decisioning

- Real-time fraud scoring

- BIN & issuer intelligence

- Smart routing (see routing guide)

- Deep integration with high-risk payment stacks

- Built-in chargeback prevention workflows

How to Roll Out 3D Secure Without Hurting Revenue

Step 1 — Audit Your Fraud & Disputes

Start with a payment performance audit.

Step 2 — Start With Adaptive Rules

Don’t blanket everything.

Step 3 — Monitor Conversion, Approval & Fraud Together

3DS must be tuned continuously.

Step 4 — Combine With Other Tools

- Network tokens

- Smart routing

- Pre-dispute alerts (see Ethoca vs Verifi).