What Is a Chargeback?

A chargeback happens when a cardholder disputes a transaction with their bank instead of asking the merchant for a refund.

While chargebacks were originally designed to protect consumers from fraud, today they are commonly caused by:

- Friendly fraud

- Confusion about billing descriptors

- Poor customer service or refund flows

- Delivery or fulfillment disputes

- Real fraud

Every chargeback costs you:

- The revenue from the transaction

- The product or service

- A dispute fee

And long-term damage to your risk profile

Why Chargebacks Are So Dangerous Today

Chargebacks no longer just cost money — they threaten your ability to accept payments at all.

If your ratios exceed card network thresholds, you can be placed into:

- Visa VAMP

- Visa Excessive or High Risk programs

- Mastercard High Fraud or High Chargeback programs

Once in these programs:

- Fees increase

- Approval rates drop

- Reserves are imposed

- Accounts get terminated

What Causes Chargebacks?

Understanding the root cause is the first step to prevention.

1. Fraud

- Stolen cards

- Account takeovers

- Card testing attacks

2. Friendly Fraud

- Customer forgets the purchase

- Family member used the card

- Subscription confusion

- Customer goes to the bank instead of you

3. Operational Issues

- Poor descriptors

- Slow shipping

- Weak refund policies

- Bad customer support

4. Technical Payment Issues

- Duplicate charges

- Retry logic gone wrong

- Authorization/capture timing issues

- Simplify Accounting and Reporting

Why Traditional Chargeback Management Fails

Most businesses focus on:

- Fighting chargebacks after they happen

But by the time a chargeback exists:

- You’ve already lost the money

- Your ratios already got worse

- The networks already counted it against you

Modern chargeback prevention focuses on:

- Stopping disputes before they become chargebacks

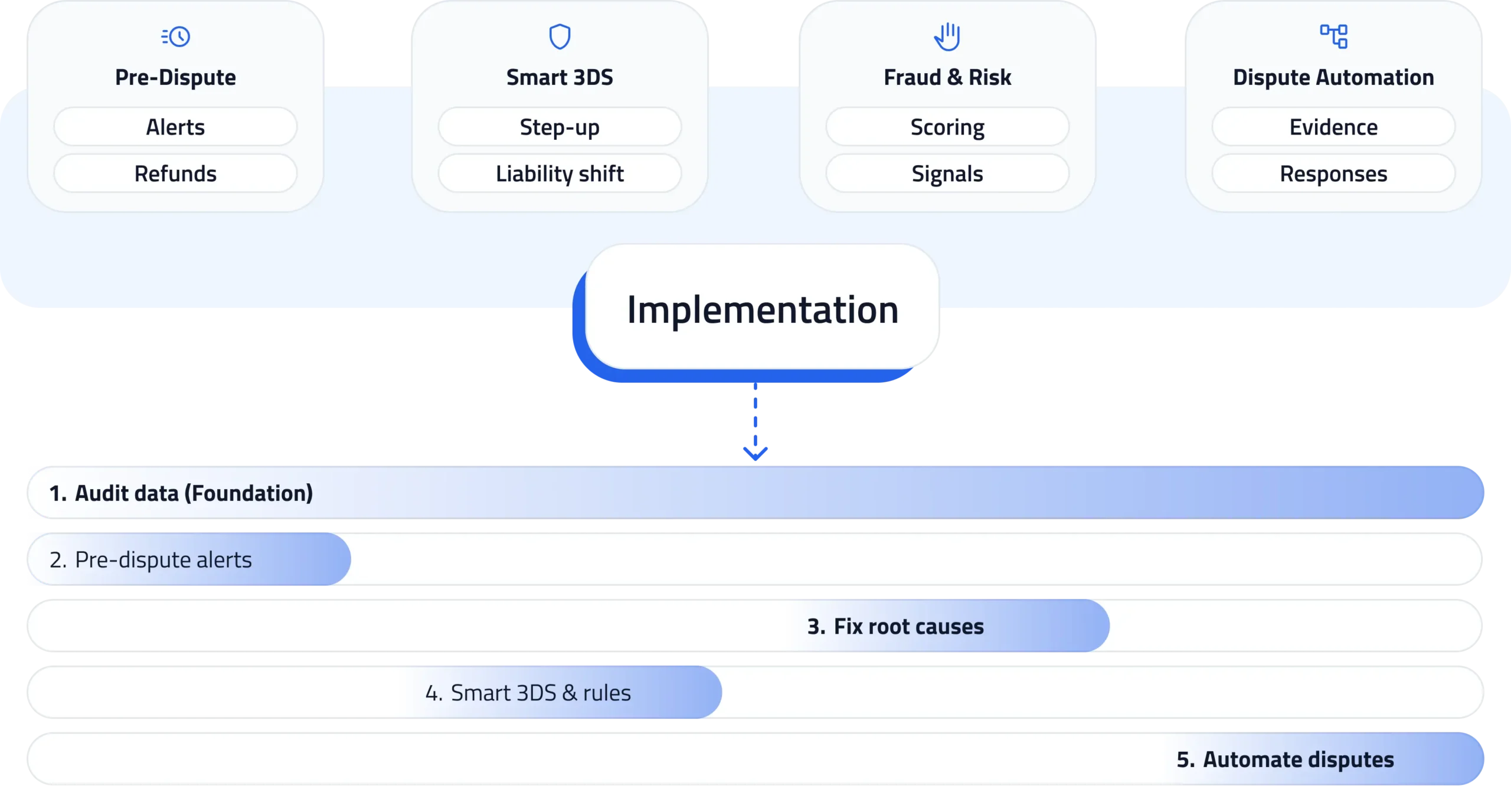

The 4 Pillars of Modern Chargeback Prevention

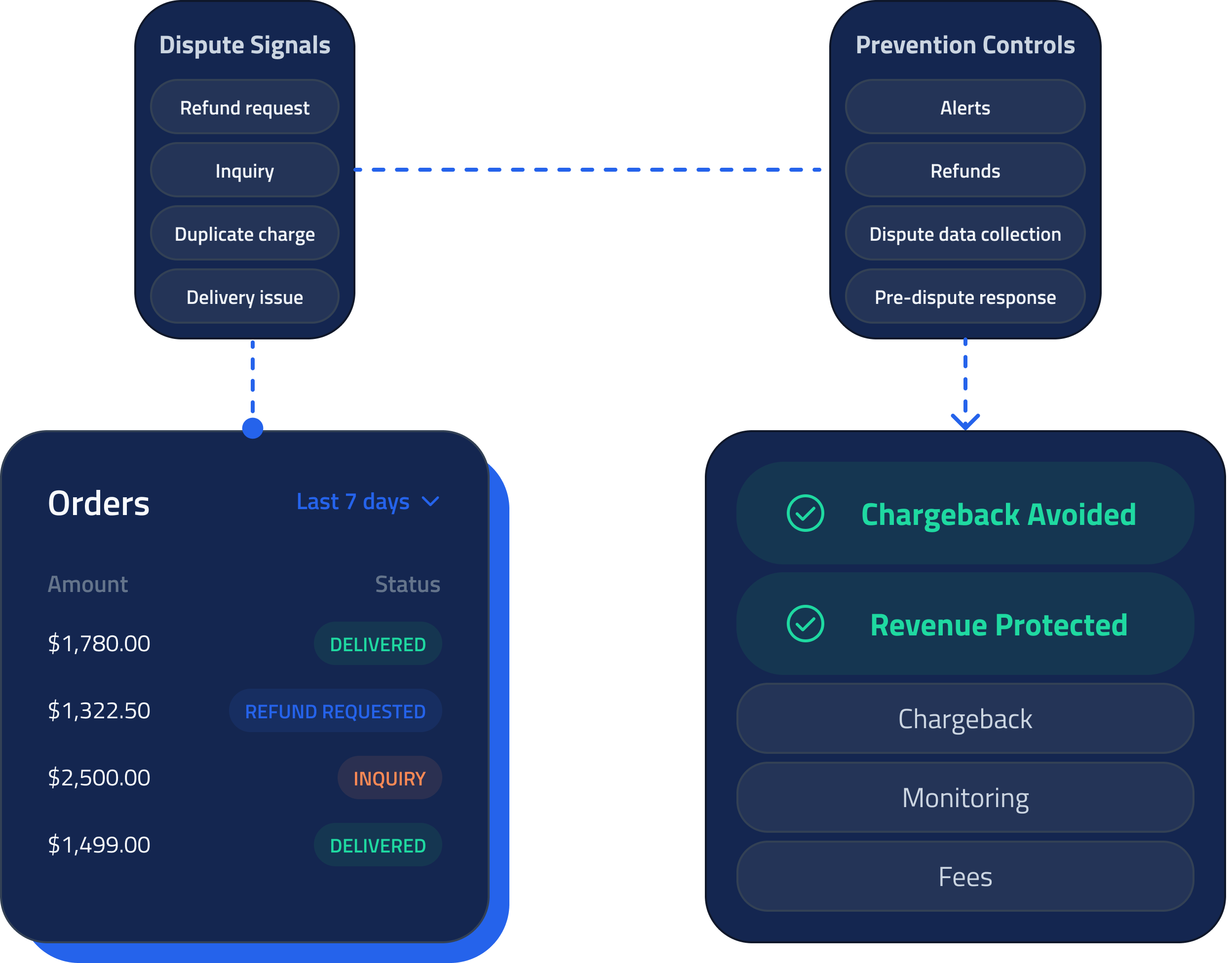

1. Pre-Dispute Deflection (Verifi & Ethoca)

Tools like:

- Verifi RDR (Visa Rapid Dispute Resolution)

- Ethoca Alerts

Allow you to:

- Detect disputes before they become chargebacks

- Refund or resolve them automatically

- Protect your ratios and monitoring thresholds

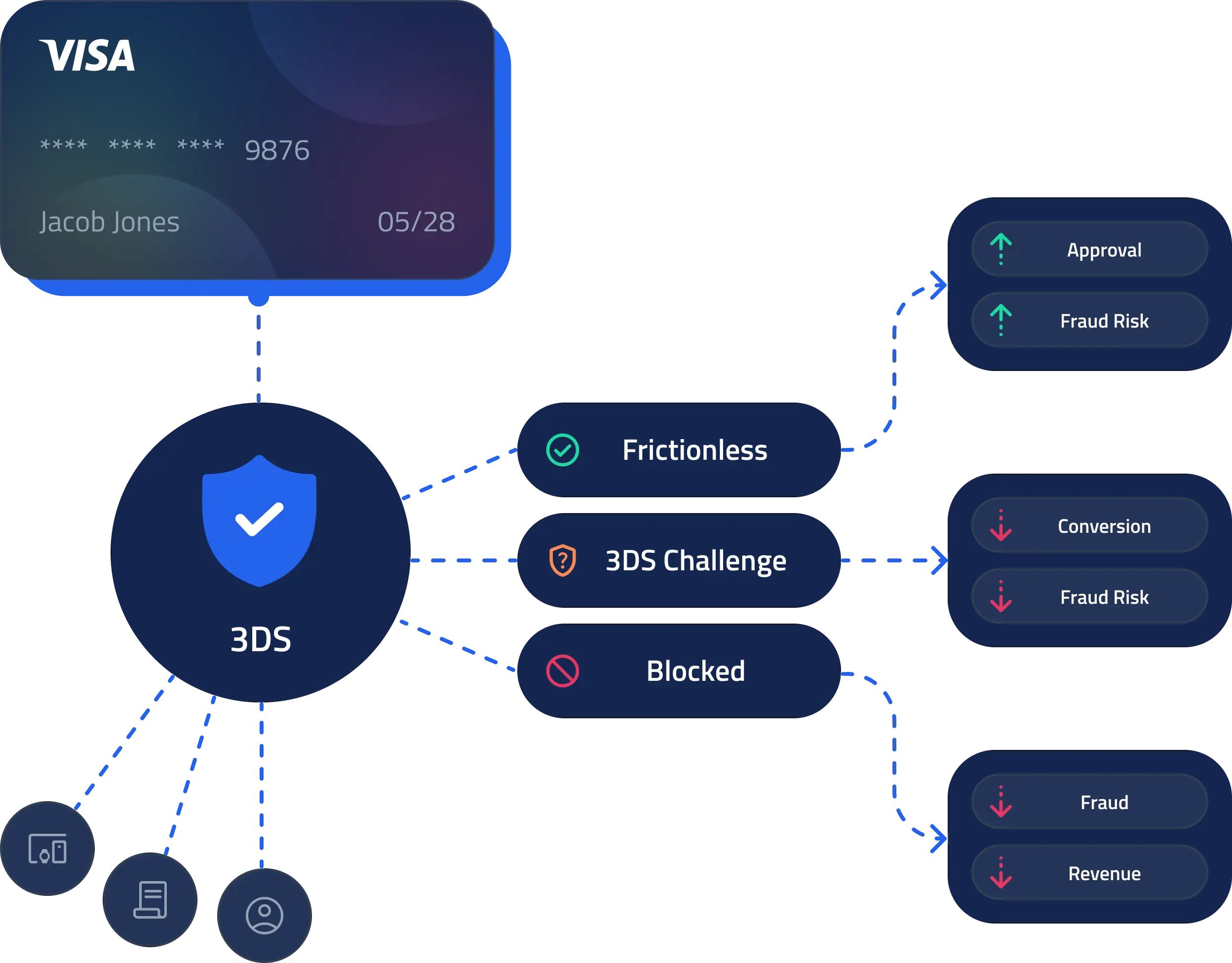

2. Smart Authentication (3D Secure)

Using adaptive 3D Secure:

- Step-up only risky transactions

- Shift liability on fraud disputes

- Reduce both fraud and friendly fraud

3. Better Fraud & Risk Decisions

Modern stacks use:

- Real-time fraud scoring

- BIN intelligence

- Velocity controls

- Geo & device fingerprinting

This prevents:

- Stolen card fraud

- Bot attacks

- Card testing

4. Dispute Automation & Evidence Quality

When disputes do happen:

- Respond automatically

- Use AI-generated evidence

- Tailor responses by reason code

- Maximize win rates

How to Reduce Chargebacks in 30–60 Days (Action Plan)

Step 1 — Audit Your Chargeback Data

Look at:

- Reason codes

- Issuers

- Products

- Traffic sources

Step 2 — Turn On Pre-Dispute Alerts

This is usually the fastest win.

Step 3 — Fix Your Top 3 Root Causes

Usually:

- Descriptors

- Refund flow

- Subscription clarity

Step 4 — Add Smart 3DS & Risk Rules

Don’t blanket everything. Be adaptive.

Step 5 — Automate Dispute Responses

Manual dispute handling does not scale.

How Many Chargebacks Are Too Many?

Most merchants should stay below:

- 0.65% dispute ratio (Visa safe zone)

- 0.9%+ = monitoring risk

- 1%+ = serious account termination risk

Chargeback Prevention Software: What to Look For

A real chargeback prevention platform should include:

- Verifi RDR + Ethoca

- Smart 3D Secure

- Fraud scoring

- Dispute automation

- Monitoring & alerts

- VAMP tracking

How SeamlessPay Helps Prevent Chargebacks

SeamlessPay is not just a dispute tool. It’s a payment performance and risk decision engine.

With SeamlessPay you get:

- Pre-dispute deflection (Verifi + Ethoca)

- AI-generated dispute responses

- Adaptive 3DS

- Real-time fraud scoring

- BIN & issuer intelligence

- VAMP monitoring and prevention

Most clients reduce chargebacks 20–50% in the first 60–90 days.